米連邦準備理事会(FRB)は2日の米連邦公開市場委員会(FOMC)で0.75%の利上げを決めました。通常の3倍の利上げ幅で、6月に約27年ぶりに実施してからは4会合連続となりました。0.75%の利上げ幅は市場予想通りで、短期金利の指標であるフェデラルファンド(FF)金利の誘導目標は3.75~4.0%となりました。

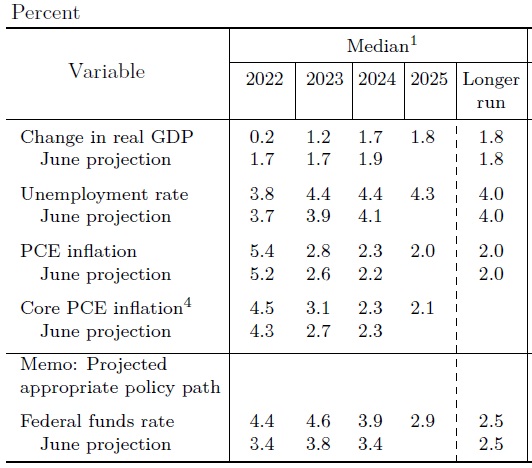

FOMC参加者が9月に示した政策金利の見通しでは、2022年末の中央値が4.4%でしたので、12月に利上げ幅を0.5%に縮める予想です。

2日に公表した声明文では経済成長は減速したものの、雇用や賃金上昇は堅確(robust)とし、以前インフレ抑制のために断固とした姿勢を取ると示した一方で、「金融政策が経済活動や物価に影響を及ぼすのに時間差(ラグ)がある点を考慮する」と文言が付け加えられました。

Despite the slowdown in growth, the labor market remains extremely tight, with the

unemployment rate at a 50-year low, job vacancies still very high, and wage growth elevated.Job gains have been robust, with employment rising by an average of 289,000 jobs per month over August and September.(略)

That’s why we say in our statement that in determining the pace of future increases in the target range, we will take into account the cumulative tightening of monetary policy and the lags with which monetary policy affects economic activity and inflation.

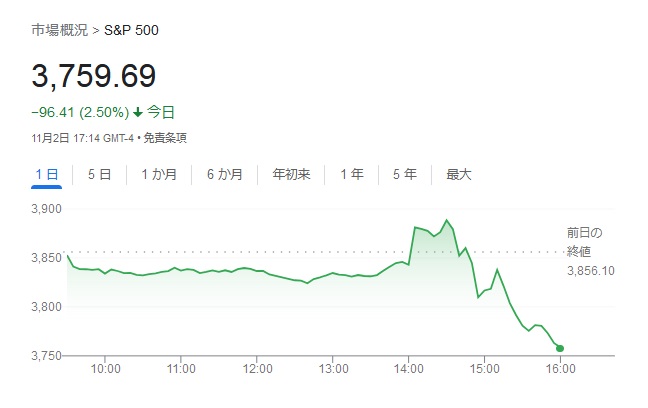

この文言を市場では引き締めペースの減速を示唆するものと捉え、一時株価が上昇したものの、その後のパウエル議長の記者会見で、その期待も打ち崩されました。

記者会見では、「金利水準は9月会合で示した水準より高くなるかもしれない」と発言し、最終的な金利水準(ターミナルレート)は従来予想よりも高くなることを示唆しました。

We still have some ways to go and incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected,

利上げペースに関しては、利上げを減速させる時期は早ければ次の会合にも到来(ただし何も決まっていない)としながらも、利上げの打ち止めを考えるのは時期尚早(premature)とコメントしました。

That’s why I’ve said it’s appropriate to slow the pace of increases,So that time is coming. And it may come as soon as the next meeting or the one after that. No decision has been made.

It is very premature to be thinking about pausing. People when they hear ‘lags’ think about a pause. It is very premature, in my view, to think about or be talking about pausing our rate hikes. We have a ways to go,

また注目している「経済と利上げのソフトランディング」については、「1年前より”narrowed”」と回答していました。

We’ve always said it was going to be difficult, but to the extent rates have to go higher and stay higher for longer it becomes harder to see the path. It’s narrowed. I would say the path has narrowed over the course of the last year.

前述のとおり、一時は「タイムラグがある」=「タイムラグを考慮して利上げペースが緩くなる」との思惑から株高に振れましたが、その後の記者会見での数々のタカ派の発言から、引けにかけて大きく下落しました。

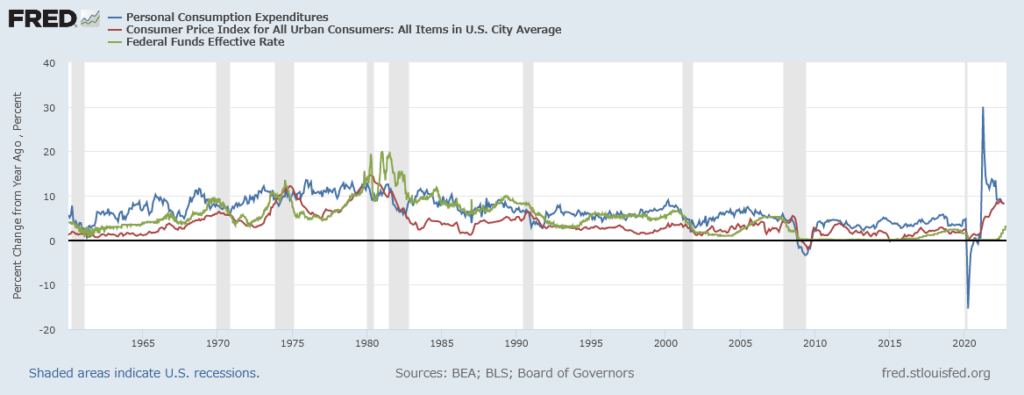

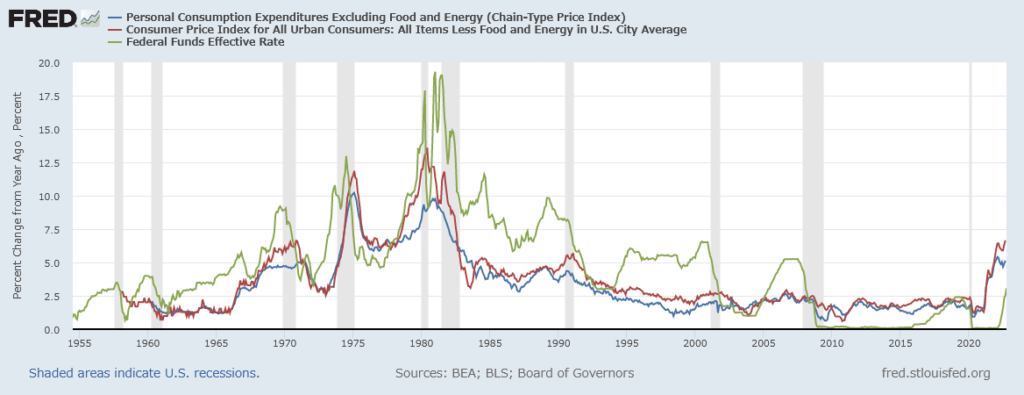

こうなってくると注目となってくるのが「ターミナルレートがいくつなのか?」です。過去を振り返ると、インフレ抑制時には物価指数(FRBが注目しているのはPCE)程度まで政策金利を引き上げているということ。コア(食品・エネルギー除く)か総合かの議論だと、総合指数のようです。

この前提に立てば、現在CPI総合もPCE総合も前年比8%程度で推移していますので、今後のタイムラグ(インフレ指標は遅行指数)を考慮しても6%~7%は見ておく必要があるとは考えています。意外と12月頃に出てくるインフレ指標が改善していてあっさり政策金利付近まで落ちて来てくれるのか、それとも”粘着質”であるため、なかなか鈍化せずに、それに政策金利を寄せに行く(引き上げる)形になるのか、まだまだ楽観視できない環境が続きます。